How Much Down Payment Do You Need to Buy a House in India?

Down Payment for a House in India is one of the most important financial considerations for homebuyers. While many people focus on home loan eligibility and monthly EMIs, the amount required as a down payment often determines whether a property purchase is feasible.

Understanding how much down payment you need can help you plan your finances effectively, reduce loan burden, and improve your chances of securing favorable loan terms.

In this guide, we explain everything you need to know about the down payment for a house in India, including lender requirements, factors affecting the amount, and practical saving tips.

What Is a Down Payment?

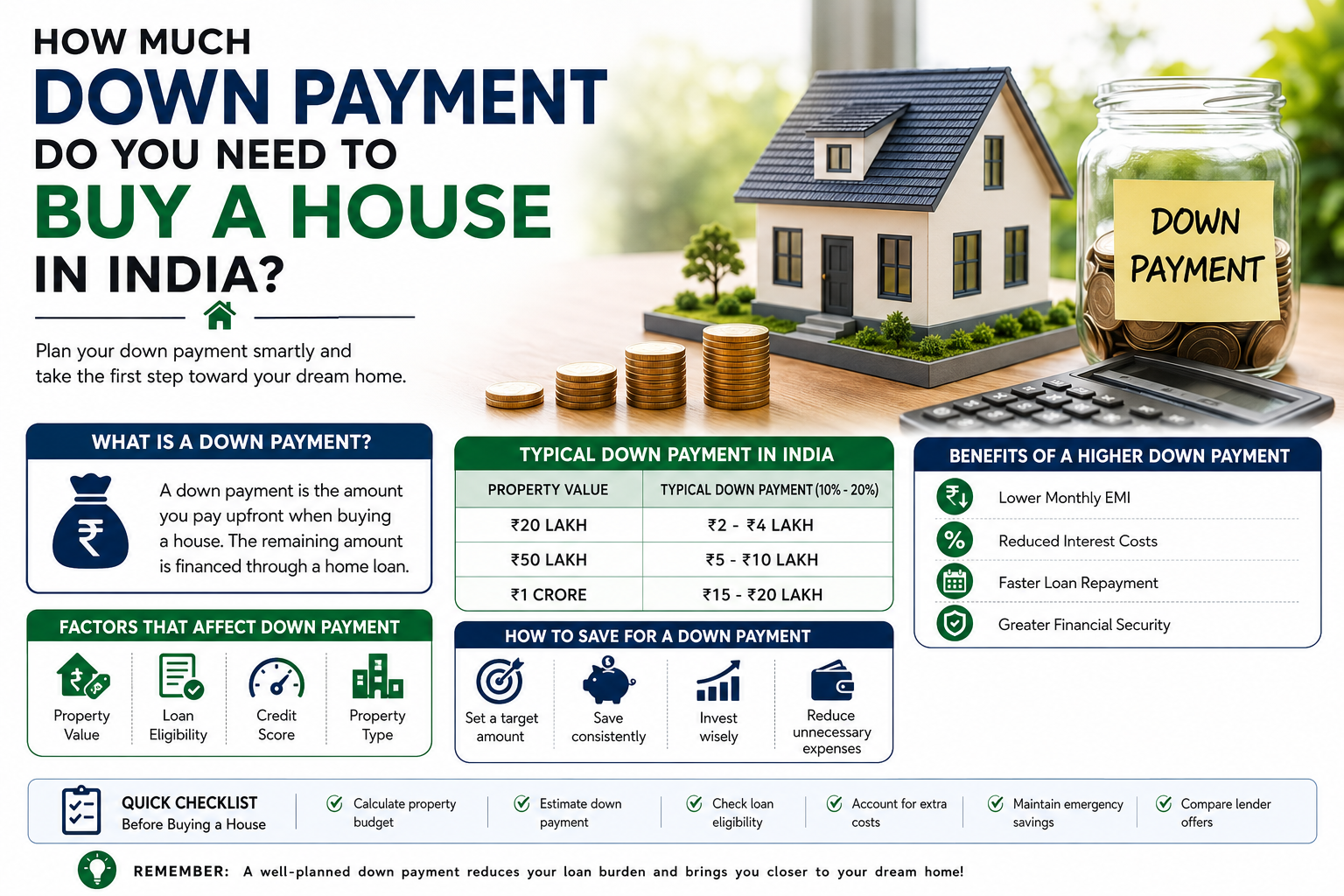

A down payment is the portion of the property’s purchase price that the buyer pays upfront from personal funds.

The remaining amount is typically financed through a home loan.

Example

Suppose a property costs ₹50 lakh.

If the lender finances 80% of the property value:

- Home Loan: ₹40 lakh

- Down Payment: ₹10 lakh

In this scenario, the buyer must arrange ₹10 lakh before obtaining the loan.

Why Is a Down Payment Required?

Lenders require buyers to contribute a portion of the property value to reduce lending risk.

Benefits of a Down Payment

- Reduces loan amount

- Lowers monthly EMI

- Improves loan approval chances

- Reduces total interest paid

- Demonstrates financial discipline

A larger down payment often results in better financial flexibility.

Minimum Down Payment for a House in India

The minimum down payment depends on the loan-to-value (LTV) ratio offered by the lender.

To understand how lenders calculate down payments, loan-to-value ratios, and home loan funding limits in greater detail, refer to this comprehensive Home Loan Down Payment Guide.

Understanding Loan-to-Value Ratio

RBI Guidelines on Home Loan Down Payments

The Reserve Bank of India (RBI) permits lenders to finance a significant portion of a property’s value through home loans. However, borrowers are generally required to contribute a minimum share as a down payment. The exact amount depends on the property’s value and the lender’s internal policies.

The LTV ratio represents the percentage of property value financed by the lender.

Typical LTV Ratios

- Up to 90% for smaller loans

- Around 80–85% for higher-value properties

- Lower percentages for luxury properties

Common Down Payment Requirements

| Property Value | Typical Down Payment |

|---|---|

| ₹20 lakh | ₹2–4 lakh |

| ₹50 lakh | ₹5–10 lakh |

| ₹1 crore | ₹15–20 lakh |

Actual requirements vary based on lender policies and borrower profiles.

Factors That Affect the Down Payment Requirement

Several factors influence how much down payment for a house in India is required.

Property Value

Higher-priced properties generally require larger down payments.

Loan Eligibility

Your income and credit profile influence how much financing the lender is willing to provide.

Credit Score

A strong credit score can improve loan terms and financing options.

Property Type

Different property categories may have different financing limits.

Benefits of Making a Higher Down Payment

Although buyers often prefer smaller upfront payments, a larger down payment offers significant advantages.

Lower Monthly EMI

Borrowing less money results in lower monthly loan payments.

Reduced Interest Costs

A smaller loan amount means less interest paid over the loan tenure.

Faster Loan Repayment

Lower debt can help borrowers become mortgage-free sooner.

Greater Financial Security

Higher equity reduces financial stress and improves long-term stability.

Should You Use All Your Savings for a Down Payment?

Many buyers make the mistake of exhausting their savings.

Why This Can Be Risky

Homeownership involves several additional expenses:

- Registration charges

- Stamp duty

- Interior work

- Maintenance costs

- Emergency repairs

Maintaining an emergency fund is essential even after making a down payment.

How to Save for a House Down Payment

Saving for a down payment requires planning and discipline.

Set a Target Amount

Determine the property budget and estimate the required down payment.

Create a Dedicated Savings Plan

Allocate a fixed percentage of monthly income toward your home-buying goal.

Reduce Unnecessary Expenses

Cutting discretionary spending can accelerate savings growth.

Invest Wisely

Appropriate investment options may help your savings grow over time.

Common Mistakes Homebuyers Should Avoid

Ignoring Additional Costs

Many buyers only plan for the down payment and overlook transaction-related expenses.

Taking Personal Loans for the Down Payment

This increases financial burden and may affect home loan approval.

Skipping Loan Preparation

Buyers should also understand Home Loan Pre-Approval before starting their property search to improve financing readiness.

Buying Beyond Budget

Avoid selecting a property solely based on loan eligibility.

Buyers should also be aware of Real Estate Scams in India and How to Avoid Them before making any property purchase, as fraud and document-related issues can lead to significant financial losses.

Choose a property that aligns with your long-term financial goals.

Down Payment Checklist for Homebuyers

Before Buying a House

- Calculate property budget

- Estimate required down payment

- Check credit score

- Review home loan eligibility

- Maintain emergency savings

- Account for registration costs

- Compare lender offers

- Plan future EMIs

Following this checklist can help buyers make informed financial decisions.

Conclusion

Down Payment for a House in India is a crucial part of the home-buying process. While most lenders finance a large portion of the property value, buyers must still contribute a meaningful upfront payment.

Understanding lender requirements, planning finances carefully, and maintaining a balanced savings strategy can help you purchase a home with confidence. By preparing for your down payment early, you can reduce financial stress and build a stronger foundation for long-term homeownership.